As a business,have you ever faced a scenario like this?Where you spend months preparing your business plan, assembling financial documents, and walking into a bank for a working capital loan—only to be told your application has been rejected.No clear explanation! No roadmap for what to fix. Just a polite “no.”

You are not alone. Thousands of business owners and MSMEs every year face such problems. The most frustrating part? One simple fix could have helped them avoid such issues i.e to check their Credit Information Report beforehand!It is very essential to keep CIR up to the mark. In this article, we break down seven compelling reasons why every Indian business—whether you are a bootstrapped startup, a growing MSME, or an established enterprise—must take their CIR seriously.

What is a Credit Information Report (CIR)?

A Credit Information Report (CIR) is a detailed record of your business’s credit history, prepared by credit bureaus like TransUnion CIBIL, Experian, CRIF High Mark, and Equifax. For Example – Think of it as your business’s financial passport—and just like a passport, you need it to be valid, accurate, and up-to-date before you travel anywhere important.

It gives lenders a complete picture of how your business has handled credit over time, including:

- Current and past business loans

- Repayment history and financial discipline

- Outstanding dues and credit limits

- Defaults, settlements, or written-off accounts

- Credit enquiries made by banks or lenders

For businesses in India, a CIR is far more than just a report. It plays a major role in deciding whether your business can access bank loans, NBFC funding, MSME schemes, or supplier credit.

A healthy CIR builds trust and shows that your business manages credit responsibly. On the other hand, a weak report can reduce your chances of getting funding — often without you even realizing why.

According to RBI data, credit penetration among MSMEs in India remains significantly low — and one key reason is poor credit visibility. Your CIR is the first step to changing that.

7 Reasons Why Your Business Needs a Credit Information Report

India’s credit ecosystem is rapidly growing due to the pace of economic growth, financial transparency is no longer optional. Lenders, NBFCs, and even suppliers are increasingly relying on credit data to make decisions.

If your business credit profile is invisible or inaccurate, you are turning every financial conversation at a disadvantage.

It’s the First Thing Lenders Check Before Approving a Loan

Whenever you apply for a business loan, banks and NBFCs usually begin by checking your Credit Information Report (CIR). This report helps them understand how responsibly your business has handled credit in the past.Your CIR directly impacts your credit score — and that score often decides whether your loan application moves forward or gets rejected early in the process.For MSME loans under schemes like CGTMSE or Pradhan Mantri Mudra Yojana, lenders closely review your repayment history and existing debts before approving funding. Businesses with a credit score above 700 usually have a better chance of getting quicker approvals, lower interest rates, and higher loan amounts.Checking your CIR beforehand helps you understand where your business stands and gives you time to fix any issues before applying for a loan.

It Helps You Spot Mistakes Before They Hurt Your Business

Credit reports can sometimes contain errors. A loan you already paid may still show as pending, or someone else’s account could accidentally get linked to your business profile. Even small mistakes like these can negatively affect your credit score without you realizing it.It Improves Your Chances of Getting NBFC Financing In India, correcting credit report errors through bureaus can take time. That’s why regularly checking your CIR is important. It allows you to identify problems early, raise disputes quickly, and make sure your report accurately reflects your financial behaviour.

It Improves Your Chances of Getting NBFC Financing

Today, many businesses rely on NBFCs for faster and more flexible funding. But NBFCs also carefully evaluate your credit profile before approving loans.A healthy CIR shows lenders that your business manages debt responsibly. It also helps them assess your current credit usage and determine how much additional funding you can safely handle.When you know your credit position in advance, you can apply for the right loan amount and avoid unnecessary rejections.

It Helps You Access Better Working Capital

Every business needs working capital to manage day-to-day operations — whether it’s buying inventory, handling delayed payments, or fulfilling a large order.Before offering facilities like overdrafts, cash credit, or invoice financing, lenders usually review your CIR. Businesses with strong credit profiles often get better loan terms, higher limits, and faster approvals.

>

On the other hand, businesses that ignore their credit profile may struggle to get emergency funding when they need it most.It Reflects GST-Linked Financial BehaviourIndia’s GST ecosystem has created an interconnected financial data trail for businesses. While GST data itself is not directly part of a Credit Information Report, lenders increasingly cross-reference your GST filing history with your CIR to build a fuller picture of your business’s financial health.

It Builds Long-Term Trust With Lenders and Suppliers

A strong business credit profile does more than help you get loans — it also strengthens your reputation in the market.Over time, businesses with a healthy CIR are seen as reliable and financially disciplined. This can help you build stronger relationships with banks, NBFCs, and even suppliers who may be willing to offer trade credit or flexible payment terms.For startups, building business credit early is especially important. Many entrepreneurs only borrow in their personal name, which means the business itself never develops an independent credit identity. Creating a strong CIR from the beginning helps your business grow with a stronger financial foundation.

It Helps You Improve Your Credit Score Strategically

You cannot improve what you cannot measure. A Credit Information Report gives you a detailed, data-backed understanding of exactly what is affecting your credit score—and in which direction.

Is your credit utilization too high? Are there too many recent loan inquiries? Do you have a short credit history? Each of these factors appears clearly in your CIR, and each one can be addressed with a targeted strategy. Businesses that regularly check and act on their CIR consistently improve their credit score over time — which directly translates into better loan terms and greater financial freedom.

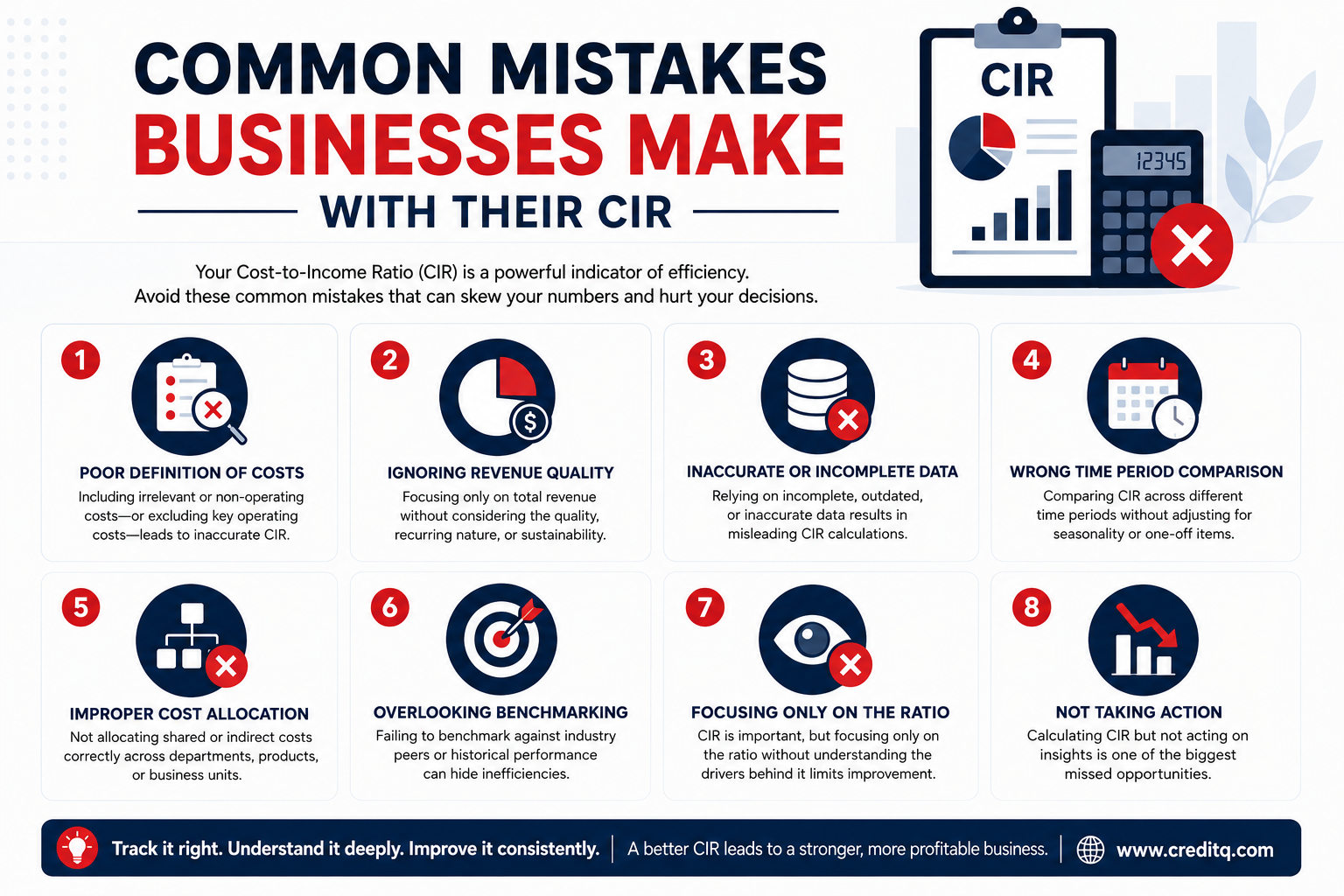

Common Mistakes Businesses Make With Their CIR

Despite the importance of credit data, many Indian businesses fall into avoidable traps that quietly undermine their financial credibility.

Not Checking the CIR Regularly

Many business owners check their credit report only when they urgently need a loan. By then, errors or damage may have already occurred. Quarterly reviews are a sound practice.

Ignoring the Impact of Late Payments

Even a single missed EMI or delayed credit card payment can leave a mark on your business credit report. Consistent, on-time repayments are the single most powerful thing you can do for your score.

Applying for Multiple Loans Simultaneously

Every loan inquiry leaves a hard inquiry mark on your CIR. Multiple inquiries in a short span signal credit-hungry behavior to lenders—and can lower your score even before any loan is disbursed.

Confusing Personal and Business Credit

Many MSMEs rely solely on the promoter’s personal credit score. Building a separate business credit identity protects your personal finances and gives your company an independent financial standing.

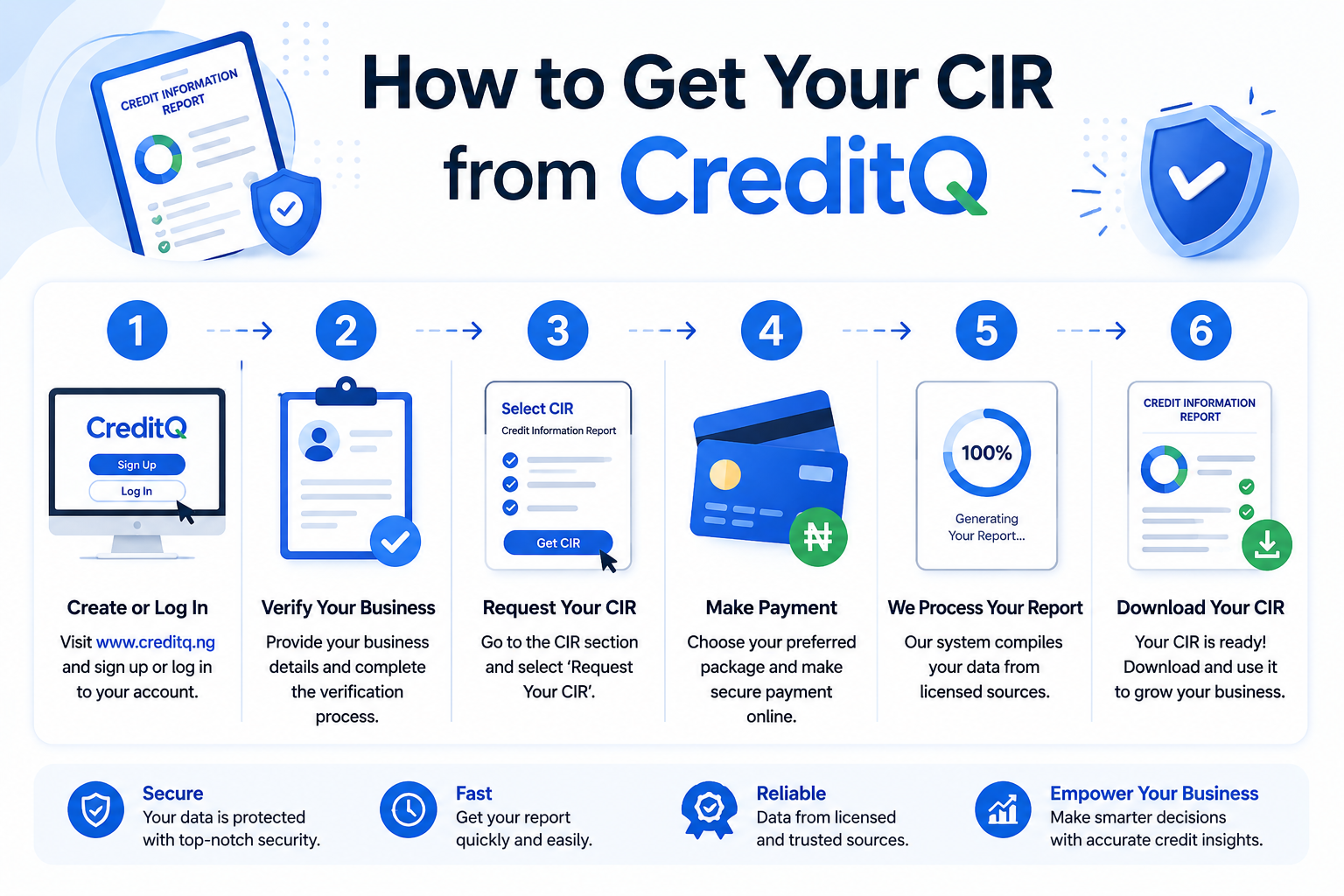

How to Get Your CIR from CreditQ

Getting your Credit Information Report does not have to be complicated. CreditQ.in has been designed specifically to make the process fast, reliable, and easy to understand — even if you are checking your business credit score for the first time.

- Visit creditq.in — Go to the official CreditQ website and navigate to the Credit Information Report section.

- Register or log in — Create your secure account using your business details. The process takes under two minutes.

- Verify your identity — Submit the required KYC documents for authentication. CreditQ follows all regulatory data protection standards.

- Access your CIR instantly—Your detailed Credit Information Report is generated and available for download within moments.

- Review and act — CreditQ presents your CIR in a clear, readable format with insights to help you understand your credit position and next steps.

What sets CreditQ apart is not just the speed of access—it is the context provided alongside your report. Rather than handing you a dense document and leaving you to interpret it alone, CreditQ offers financial insights that help you understand what your credit data actually means for your business’s future.

Conclusion

Your business’s financial story is being told every day—through every EMI paid, every loan taken, and every payment made on time or delayed. A Credit Information Report is the written version of that story, and the question is: are you the one reading it, or are you letting lenders read it first?

From unlocking MSME loan approvals and NBFC financing to building long-term supplier credibility and strategically improving your credit score, the CIR is one of the most actionable financial tools available to Indian businesses today — and it is often the most overlooked.

The most financially aware business owners in India are not the ones who borrow the most — they are the ones who know their numbers, monitor their credit profile, and make informed decisions before anyone else has a chance to make decisions about them.

Your CIR is not just a report. It is your financial reputation—and it is worth taking seriously.

Frequently Asked Questions

1. What is a Credit Information Report (CIR) for a business?

A business Credit Information Report shows credit history, repayments, loans, and dues to assess financial reliability and trustworthiness.

2. How is a business CIR different from a personal credit report?

A personal report tracks individual borrowing, while a business CIR tracks company loans, keeping personal and business finances separate.

3. How often should a business check its Credit Information Report?

Ideally, businesses should review their CIR at least once every quarter. If you are planning to apply for a loan or credit facility in the near future, it is advisable to check your CIR two to three months in advance so you have time to address any issues or errors.