Managing commercial risk is one of the most critical elements for survival and long-term business growth. Most deals between buyers and suppliers are done on credit terms. This means business owners are frequently confronted with the possible danger of late payments or bad debts. A reliable business credit report is a primary tool to verify the credibility of a client before signing any deal. Reviewing a company’s previous behaviors can give your company clarity on whether a buyer will meet their financial obligations or become a default liability. True financial insights are being delivered by professional platforms such as CreditQ, revolutionizing how small and medium businesses handle these operational risks.

Offering products or services on credit without looking at data is like playing games with your cash flow. One bad deal can wipe out your working capital, disrupt your supply chain and bring your normal operations to a halt. This in-depth guide will show you how a structured commercial check can help protect your cash flow, protect your profit margins and protect your long-term operational safety.

What is a Commercial Profile?

A Corporate Profile is a compiled document that amalgamates the complete payment behavior and transaction history of a commercial entity. This document is the analysis of the relationship between companies, official records of the market and previous trades. Such vital information is collected by platforms such as CreditQ from official data sources, certified and direct updates from the registered business members.

The resulting profile is an objective picture of a firm’s operational reliability. Sellers get to see real signs of corporate stability instead of relying on word-of-mouth references or superficial corporate presentations. It indicates transaction activities and whether the company is meeting the timelines it has committed to or is consistently delaying payments to its trade vendors.

The True Cost of Late Payments and Defaults

Late payments are not just inconveniences for Micro, Small and Medium Enterprises; they are serious operational bottlenecks. Your capital is tied up and you have to use your own money to keep your business going when your buyer pays you late, after the due date.

A delay like that can become a full-blown default on the payment, and the financial damage can be permanent. Writing off bad debt comes right out of your bottom line. You need a lot of future sales to make up for the original loss. On top of that, chasing unpaid invoices consumes valuable time and energy that your team could spend on developing the core business and on revenue-generating activities.

Real Benefits of a Business Credit Report Review

One of the most clear benefits of reviewing a verified business credit report is finding out about a client’s previous defaults in repaying loans. It shows exactly how many suppliers have previously highlighted that particular buyer for non-payment / extreme delays. Identifying these red flags early can help you avoid risky deals before inventory even leaves your warehouse.

Not every client receives the same credit time frame or financial threshold. A business credit report can help you to evaluate a company’s financial capacity and set safe trading limits. For example, a buyer with a great track record could get favorable terms, while a company with spotty data could be limited to prepayments or shorter payment schedules.

And when you have clear, objective corporate data, you’re ahead of the game in contract negotiations.” If a potential customer demands extended terms and has a history of poor payment, it’s easy to change the conversation to more reasonable parameters. You can back up your terms with facts, suggesting milestone-based billing or cash-on-delivery options to protect your capital.

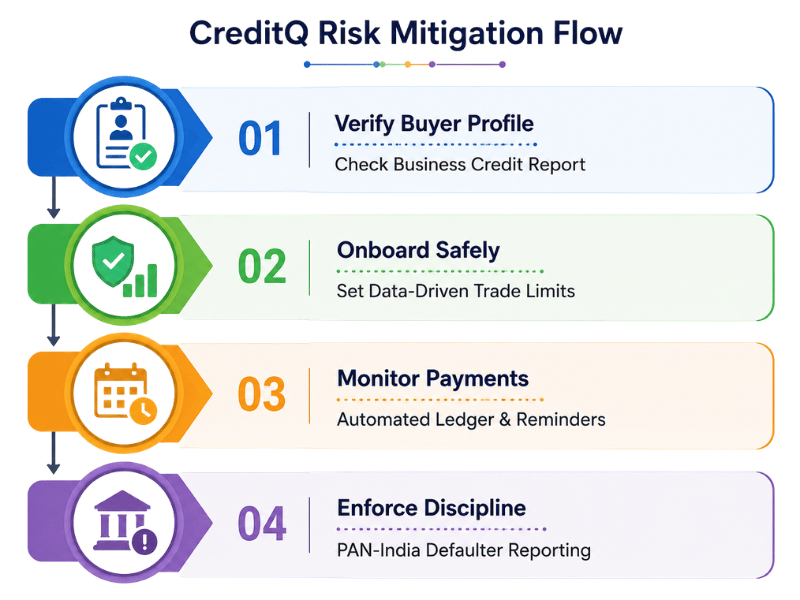

How CreditQ Transforms Risk Management

The modern way to handle risks is not manual follow-ups like in the old days, but automated digital tools. CreditQ is a digital platform which functions as a specialized ecosystem for business management and information, specifically designed to enable suppliers to easily monitor, manage and secure their credit transactions.

The platform integrates seamlessly with popular business GST. Once an invoice is uploaded, the platform automates the digital acknowledgment between buyers and suppliers to ensure both parties agree to the terms. It automatically sends alerts before and after the due date for late payments, so that there is no need for uncomfortable manual phone calls. In case the buyer still refuses to pay, users can report them as a defaulter at a PAN India level, which directly reduces the buyer’s visibility and pushes them towards a quick settlement.

Proactive Measures to Protect Business Cash Flow

“Building a defense wall alone is not enough; companies need to foster a culture of financial discipline in all their trade relationships.

Formal corporate policies: Develop internal policies on who is eligible for deferred terms and SOPs on following up overdue bills.

Use Automated Reminders: Close manual communication gaps with system-driven alerts that automatically remind clients of upcoming deadlines.

Implement Strict Penalty Clauses: Be clear in your original contracts that you will apply interest charges or late fee conditions.

Conduct Regular Reviews: A financially sound business today can have cash flow problems tomorrow, so ongoing monitoring is critical to long-term safety.

Must Read: How Company Credit Reports and Auto Payment Reminders Improve Business Cash Flow

Final Summary

Companies need to stop making gut-feeling business decisions and start using verified information to avoid payment defaults. Transparency is required to filter out high-risk buyers and identify reliable, long-term trade partners, and a review of a company’s payment history provides that transparency. With digital ecosystems like CreditQ integrated into daily workflows, you can take advantage of automated ledger management, proactive alerts, and national default reporting tools. This proactive approach protects your capital, protects your cash flow and allows your enterprise to grow without the risk of unexpected financial shocks.

Frequently Asked Questions

Q1. What information is contained in a corporate payment history?

Ans: The detailed report also includes the company’s registration details, past payment history trends, active trade balances, current stability scores and legal disputes. Importantly, it reveals whether any of the other vendors have formally complained to the business about previous defaults or non-payment issues.

Q2. How does CreditQ help businesses address overdue payments?

Ans: CreditQ helps by sending professional reminders to the buyer automatically before and after the payment due date. If the buyer does not pay the invoice, the supplier can mark him as a defaulter on the national platform, which lowers his credibility in the market as a whole and encourages him to pay the debt.

Q3. How can a business report a defaulter without any documentation?

Ans: If you use the business management tools on the platform and if there are no trade disputes, you can straight away report a defaulter with a digital acknowledgement. However, in case of any dispute, you will have to submit a ledger statement and a Chartered Accountant certificate with a valid Document Identification Number for the process of reporting to be completed.

Q4. Does looking at a client’s history save an enterprise from legal issues?

Ans: Yes, by reviewing records, you can avoid companies in insolvency, in litigation, or under serious operational stress. It allows you to catch these problems early, save your business a lot of legal costs, and avoid lengthy litigation.

Q5. Why do MSMEs need to focus on business performance scores, rather than individual consumer scores?

Ans: Consumer scores are based only on the habits of a given individual, like personal utilities. A dedicated business record tracks commercial trade interaction, supplier relationships and corporate debts. It is the only accurate tool to assess B2B transaction risks.